.svg)

Everyone spent the last month asking what Salinas would look like. The transition happened. Salinas-Watsonville showed up in the USDA produce report for the first time this season. We are a few days in. Here is what is actually happening and what we think the rest of the season looks like.

The opening read.

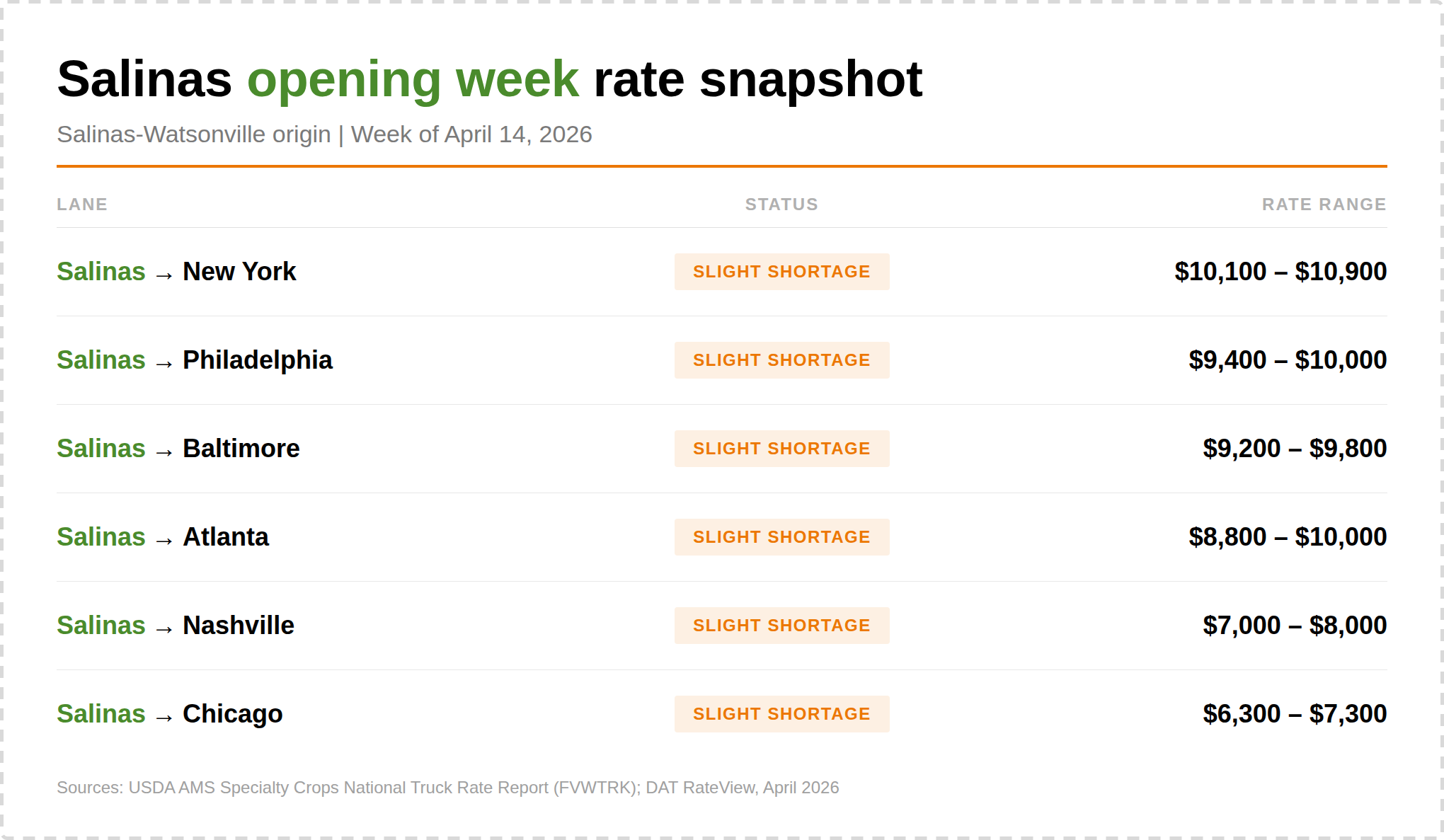

Salinas opened short on trucks across every reported commodity: broccoli, cauliflower, lettuce, strawberries, and more [1]. East Coast lanes are already commanding $9,200 to $10,900 per load. Atlanta is $8,800 to $10,000. Nashville is $7,000 to $8,000. Chicago is $6,300 to $7,300.

For context, the national reefer load-to-truck ratio (LTR) is running around 16:1 with linehaul averaging ~$2.39 per mile [2]. In the San Francisco market, which covers Salinas, LTR is already trending in the high 20s to low 30s. Not surprising for the first week of the transition, but worth paying attention to.

On the ground we are hearing…

Carriers are still holding out as long as possible to get the highest rate and are not prebooking far in advance, even with a slight week-over-week settle and a small uptick in California reefer capacity. Fall-off rates are elevated, usually because a carrier found a higher-paying load. Long wait times at the sheds are compounding the rate pressure, with carriers adding detention and layover on top of linehaul.

Salinas capacity doesn't travel.

Salinas draws from a smaller, more localized carrier pool. Smaller fleets, owner-operators, regionally committed. The big national reefer carriers stay out of produce because it’s high risk. Unlike South Texas where carriers come down from Dallas, or Florida where Georgia trucks drive east, Salinas does not pull capacity from neighboring regions. Portland and PNW carriers are not coming down to run lettuce.

What you see in the first week is close to what you get for the season. The capacity is either here or it is not.

The compliance overhang.

We covered this extensively in our previous publications, so we will keep this brief. The regulatory dynamics that reshaped capacity during Yuma have not reversed.

California’s DMV canceled approximately 13,000 non-domiciled commercial driver’s licenses in early 2026 after FMCSA identified systemic compliance violations [3]. The federal non-domiciled CDL Final Rule took effect March 16, limiting eligibility to H-2A, H-2B, and E-2 visa holders [4]. Stricter ELP enforcement has placed tens of thousands of drivers out of service since June 2025.

The direct consequence for Salinas: long-haul team capacity is effectively gone. Team driving historically relied on the same immigrant driver population these enforcement actions are removing. That pipeline has been severed. For shippers moving produce from Salinas to the East Coast on 2,500+ mile lanes, the team shortage is the reason Philadelphia, Baltimore, and New York are opening at $9,000 to $11,000.

On the plus side, some carriers who refused Yuma or South Texas this winter are willing to do Salinas. That helps at the margins. But it is a marginal gain against a structural loss.

The wildcard: California diesel

National average diesel is $5.68 per gallon. In California, it is $7.73 [5]. Fuel is roughly 21% of a carrier’s cost per mile. At California prices, rate floors are structurally higher here than anywhere else before the truck rolls.

California lost 17.5% of its refining capacity with the Phillips 66 and Valero closures [6]. That supply gap is not coming back. Surcharges lag behind reality. If your fuel tables are indexed monthly, the gap between what you are paying carriers and what it actually costs to move a load out of Salinas is widening every week.

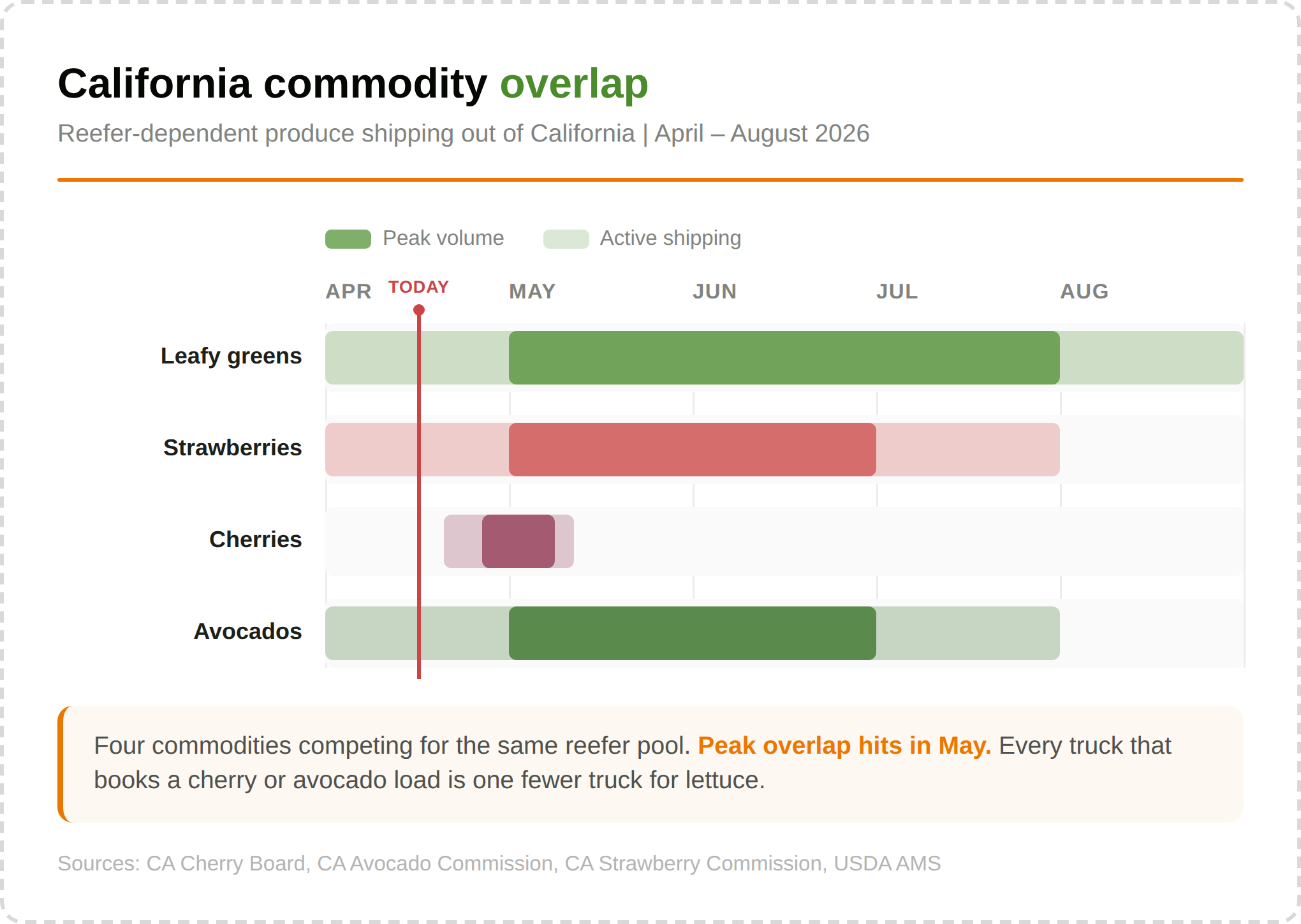

California volume is stacking up.

California accounts for roughly 20% of all U.S. produce shipments in Q2, moving 1.82 million tons last year [7]. That volume is building again, and nearly every major commodity is ramping at the same time.

Cherry harvest is beginning early, weeks ahead of the normal mid-May start. A March heat dome compressed the bloom from Bakersfield through Sacramento, and peak volume is expected in early May [8]. California avocados are projecting a record 330-million-pound crop, with peak harvest running April through August [9]. Strawberries are already shipping out of Salinas-Watsonville with volume increasing weekly. Working against all of it: the last few weeks have turned cool and wet in California, and growers are expecting yield setbacks even though the season started ahead of schedule. Lower yields per acre mean longer dwell times at the sheds and more service disruption on typical transit.

All of these draw from the same reefer pool. Every cherry, avocado, or strawberry load that commands a truck is one fewer truck for leafy green shipments.

What it comes down to.

This is not Yuma’s explosive 40-to-1 load-to-truck ratio…hopefully. Salinas does not spike the same way because it does not have the same regional dynamics. But the constraint is structural, not seasonal. The carrier pool is small and is not expected to expand. Diesel price volatility adds uncertainty. Compliance pressure keeps flex capacity out. And capacity demand for cherry, avocado, and strawberry volume is layering on top of leafy greens earlier than usual.

Salinas freight rewards preparation and punishes delay. The shippers who locked in coverage before the transition are running freight. The ones shopping spot are paying for it, especially on long-haul East Coast lanes.

We have been running Salinas produce for years. Overwhelmed sheds, rolling appointments, compressed pickup windows. We know the drill. We communicate early, work it out with the shed and the carrier, and keep your freight moving. That is what produce experience looks like when the valley gets busy.

If you are feeling the squeeze or want a second set of eyes on your Central Coast coverage, we are easy to reach.

Sources:

[1] USDA AMS. Specialty Crops National Truck Rate Report (FVWTRK). https://www.ams.usda.gov/mnreports/fvwtrk.pdf

[2] DAT Freight & Analytics. (2026, April 14). Reefer produce report. https://www.dat.com/blog/reefer-produce-report-salinas-is-open-yakima-explodes-and-nogales-cools-the-spring-transition-is-here

[3] Federal Motor Carrier Safety Administration. Non-Domiciled CDL 2026 Final Rule FAQs. https://www.fmcsa.dot.gov/regulations/non-domiciled-cdl-2026-final-rule-faqs

[4] Federal Motor Carrier Safety Administration. (2026, February 13). 91 FR 7044. https://www.federalregister.gov/documents/2026/02/13/2026-02965/restoring-integrity-to-the-issuance-of-non-domiciled-commercial-drivers-licenses-cdl

[5] AAA. (2026, April 14). AAA gas prices. https://gasprices.aaa.com/

[6] Breakthrough Fuel. How to Navigate the Impact of Closing Oil Refineries in California. https://www.breakthroughfuel.com/blog/how-to-navigate-the-impact-of-closing-oil-refineries-in-california/

[7] U.S. Department of Agriculture, Agricultural Marketing Service. Refrigerated Truck Quarterly, Q2 2025. https://www.ams.usda.gov/sites/default/files/media/RTQ2ndQuarter2025.pdf

[8] The Packer. (2026, April 2). California cherry season. https://www.thepacker.com/news/californias-cherry-season-shifts-high-gear-weeks-ahead-schedule

[9] California Avocado Commission. (2026). Pre-season crop estimate. https://www.californiaavocadogrowers.com/articles/2026-pre-season-california-avocado-crop-estimate-and-harvest-projections-available